I still remember the first time I heard the phrase “Your offer is contingent on financing approval.” I was staring at my first home purchase contract, nodding like I understood, but in my head, I was thinking, Contingent on what now? If you’ve ever found yourself in a similar moment of confusion, don’t worry—you’re not alone. Understanding what is contingency in real estate can make the difference between a smooth closing and a costly mistake.

These little clauses may look like legal jargon, but they’re the safety nets of the real estate world. They protect buyers (and sometimes sellers) from financial surprises, hidden home issues, or deals that just don’t go as planned.

What Exactly Is a Contingency in Real Estate?

A contingency in real estate is like a condition that must be met for a deal to move forward. Think of it as a “pause button” on your contract. The sale only becomes legally binding when those conditions are fulfilled.

For example, if your offer says the purchase is contingent on financing, it means the deal depends on you securing a mortgage. If you can’t get the loan, you can back out without losing your earnest money deposit.

Contingencies usually come with deadlines, too—miss them, and you might forfeit your rights to use them. They bring structure, fairness, and flexibility to what could otherwise be a stressful process.

Why Are Contingencies So Important for Home Buyers?

Here’s the truth: without contingencies, buying a home is a huge risk. You could lose your deposit or end up stuck with a house full of hidden problems.

Contingencies give you breathing room to make sure you’re making a smart investment. They let you:

- Cancel the deal if financing falls through.

- Request repairs or renegotiate after an inspection.

- Walk away if the property value doesn’t match the price.

I once watched a friend lose thousands in a deposit because she didn’t include the right contingencies in her offer. Ever since, I always tell new buyers—these clauses aren’t optional; they’re essential.

What Are the Most Common Contingencies in Real Estate?

You might wonder which conditions most buyers include. Here are the heavy hitters you’ll see in almost every contract.

1. Financing (Mortgage) Contingency

This is your safety net if your loan doesn’t go through. It gives you time to apply for a mortgage and ensures you’re not obligated to buy if financing isn’t approved.

2. Home Inspection Contingency

This one’s a lifesaver. It lets you hire a professional to check for hidden issues like structural damage, mold, or electrical problems. If something major pops up, you can ask for repairs, negotiate the price, or back out completely.

3. Appraisal Contingency

If your lender’s appraisal comes in lower than the agreed price, this clause lets you renegotiate or cancel. Since banks only lend up to the appraised value, it protects you from overpaying.

4. Title Contingency

Imagine buying a home only to find out there’s a lien or ownership dispute later. This clause allows a title search to ensure the seller legally owns the property.

5. Home Sale Contingency

Perfect for buyers who need to sell their current home first. It gives you time to secure funds before committing. Sellers often add a “kick-out clause,” allowing them to accept another offer if you can’t sell fast enough.

6. Homeowners Insurance Contingency

Some homes are hard to insure due to flood zones or old wiring. This clause ensures you can get coverage before sealing the deal.

How Does a Contingency Actually Work in a Real Estate Deal?

When a buyer includes contingencies in an offer, the seller must agree to them before the contract is signed. Once both sides are on board, the clock starts ticking on each contingency deadline.

Here’s a quick breakdown:

| Step | What Happens | Outcome if Not Met |

| Buyer adds contingencies to offer | Seller reviews and accepts | Contract becomes conditional |

| Buyer works to satisfy each condition (inspection, financing, etc.) | Seller cooperates | Deal moves toward closing |

| Condition not met (e.g., loan denied, bad inspection) | Buyer can cancel or renegotiate | Earnest money usually refunded |

If all contingencies are cleared, the status changes from “Contingent” to “Pending,” meaning you’re almost at the finish line.

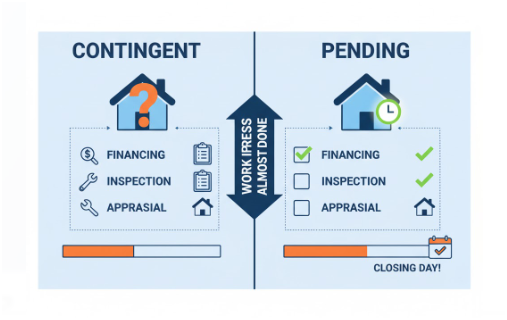

What’s the Difference Between Contingent and Pending in Real Estate?

People often confuse these terms, but they’re not the same.

A contingent property means an offer has been accepted, but the deal still depends on certain conditions. Maybe the buyer’s waiting for loan approval or a home inspection report.

A pending property means all those boxes have been checked—financing approved, inspections passed, title cleared—and now everyone’s just waiting for the final closing.

Think of “contingent” as a “work in progress” and “pending” as “almost done.”

How Can You Use Contingencies Smartly as a Buyer?

Using contingencies strategically can save you time, money, and headaches. My personal rule? Never waive them unless you’ve done your homework.

For instance, if you’re buying in a competitive market, you might feel pressured to skip inspection or appraisal contingencies to make your offer stand out. But skipping them could cost you big later.

Here’s what I suggest:

- Stay within deadlines. Missing a contingency deadline can void your protection.

- Work closely with your agent. They can help you craft clear terms that balance flexibility and security.

- Prioritize the big three. Financing, inspection, and appraisal contingencies cover most risks.

FAQs About What Is Contingency in Real Estate

1. What happens if a contingency isn’t met?

If a contingency isn’t met, the buyer can usually cancel the contract without losing their earnest money. For example, if your financing falls through, you can back out safely—as long as you’ve followed the proper steps and deadlines outlined in the contract.

2. Can a seller back out of a contingent offer?

Yes, but it depends on the terms. If the buyer fails to meet the contingency deadlines, the seller can cancel the agreement or use a “kick-out clause” to accept a backup offer.

3. Are contingencies negotiable?

Absolutely. Buyers and sellers can negotiate which contingencies to include and how long each one lasts. For instance, a seller might agree to a 10-day inspection window instead of 15 to speed things up.

4. Should I ever waive contingencies to win an offer?

Only if you’re certain about the property’s condition and your financial situation. Waiving them can make your offer stronger in a hot market, but it removes key protections if things go wrong. Always discuss the risks with your agent first.

Wrapping It Up With a Real Estate Reality Check

Understanding what is contingency in real estate can transform how you approach buying a home. It’s not just about adding clauses—it’s about protecting your investment and peace of mind.

Here’s my golden advice: treat contingencies as your safety gear in the fast-paced race of home buying. Sure, they might slow you down a little, but they’ll save you from a crash later. Every smart buyer I’ve worked with used contingencies wisely—and they slept better for it.