I still remember my first year as a real estate agent — eager, over-caffeinated, and completely overwhelmed by the financial jargon thrown my way. My broker kept mentioning “GCI” during meetings, and I nodded like I knew what it meant.

Spoiler: I didn’t. It wasn’t until my first commission check came in that I finally asked, “What is GCI in real estate, and why does everyone care so much about it?”

That question changed how I viewed my entire business. GCI, or Gross Commission Income, is more than just a fancy acronym—it’s the heartbeat of your career as an agent. Once I understood it, I could actually plan my income, manage my expenses, and measure my growth like a pro.

What Exactly Is GCI in Real Estate?

Simply put, GCI (Gross Commission Income) is the total amount of commission you earn from sales before paying for anything else. Think of it as your “top-line” number — it shows your revenue, not your profit.

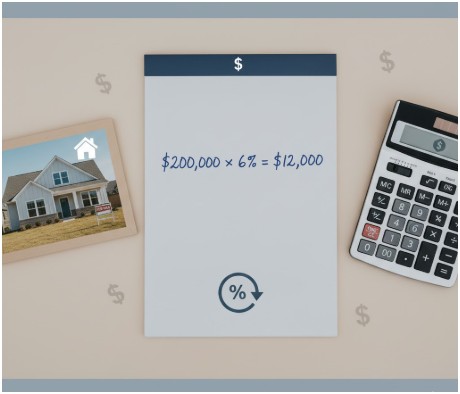

Let’s say you sell a home for $200,000 and the commission rate is 6%. You’d calculate your GCI like this:

| Sale Price | Commission Rate | GCI |

| $200,000 | 6% | $12,000 |

So, your GCI is $12,000 on that deal. But here’s the catch: you won’t pocket that full amount. You’ll still have to share it with your broker, pay your marketing costs, and cover taxes.

Understanding GCI gives you a realistic picture of your business’s health. It’s not about bragging rights—it’s about knowing your numbers so you can plan smarter.

Why Should You Care About GCI in Real Estate?

When I started tracking my GCI, I stopped guessing and started strategizing. GCI acts as your personal scoreboard. It tells you:

- How much total commission you’re generating

- Whether your business is growing year over year

- How close you are to your financial goals

For instance, if your yearly income goal is $100,000, and your average GCI per sale is $10,000, you know you need at least 10 transactions to hit that number. Suddenly, your goals become concrete instead of abstract wishes.

Beyond motivation, GCI also helps with budgeting. Once you know your gross income, you can plan for taxes, marketing costs, continuing education, and even personal savings.

How Do You Calculate GCI in Real Estate?

I promise, it’s easier than it sounds. The formula for GCI is:

GCI=Total Sale Price×Commission RateGCI = \text{Total Sale Price} \times \text{Commission Rate}GCI=Total Sale Price×Commission Rate

For example:

If you close a deal on a $500,000 home with a 5% commission, your GCI is:

500,000×0.05=25,000500,000 \times 0.05 = 25,000500,000×0.05=25,000

Your Gross Commission Income on that sale is $25,000.

However, if you’re part of a brokerage, you’ll split that amount. Suppose your broker takes 30%, you’d keep $17,500 before other expenses.

This clarity is empowering—it helps you forecast real earnings and set smarter targets.

How Does GCI Differ From Take-Home Pay?

Here’s the biggest misconception I had early on: GCI is not your paycheck. It’s your gross, not net, income.

Imagine you earned $12,000 in GCI from a sale. After splits, fees, and taxes, your actual take-home might be closer to $6,000–$8,000. The difference between the two can be shocking if you’re not prepared.

That’s why top agents always track both GCI and net income. The former shows performance; the latter shows sustainability. GCI gets you in the door, but how you manage your expenses keeps you in the game.

How Can You Use GCI to Plan Your Real Estate Career?

I use my annual GCI as a roadmap. It helps me decide how much to reinvest in my business and when to scale. Here’s how you can apply it too:

- Set income goals: Decide how much you want to earn and work backward from your average GCI per sale.

- Monitor performance: Track your GCI quarterly or monthly to see trends and seasons that perform best.

- Adjust strategy: If you’re not meeting your GCI targets, analyze your conversion rates, marketing, or pricing approach.

It’s like having a financial GPS for your real estate journey—you’ll always know whether you’re moving in the right direction.

How-To: Use GCI to Grow Your Real Estate Business

When I first realized how powerful GCI tracking was, I created a simple spreadsheet to monitor every transaction. You can do the same or use real estate CRM tools that calculate GCI automatically. Here’s a quick method that’s worked for me:

- List all your sales with sale prices and commission rates.

- Calculate GCI for each deal using the formula.

- Add up your total GCI for the month or year.

- Subtract splits, fees, and taxes to see your real profit margin.

This process helped me catch where money was slipping through the cracks. I learned to negotiate better splits and budget my marketing more wisely—all from understanding GCI.

FAQs About What Is GCI in Real Estate

1. Is GCI the same as net income?

Not at all. GCI shows your gross earnings from commissions before expenses, broker splits, or taxes. Net income is what you actually take home after those deductions.

2. How much of my GCI should I expect to keep?

It depends on your brokerage agreement and expenses, but many agents retain around 50–70% of their GCI. The rest goes toward broker fees, marketing, and taxes.

3. Why do real estate companies track GCI so closely?

Because GCI is a clear measure of productivity. It shows how much total business an agent generates, regardless of market fluctuations or expenses.

4. Can a higher GCI guarantee higher profits?

Not necessarily. You can have a high GCI and still lose money if your expenses spiral out of control. The key is balancing strong revenue with efficient cost management.

The Bottom Line: GCI Isn’t Just a Number—It’s Your Business Pulse

Here’s my take after years in real estate: understanding what GCI in real estate really means can transform your entire career. When you see GCI as more than a figure on paper, it becomes a guide—showing you when to push harder, when to scale, and when to refine your systems.

If you’re serious about building longevity in this business, don’t just chase commissions—track your GCI like your livelihood depends on it. Because, in many ways, it does.

Pro Tip: Review your GCI monthly and celebrate your milestones, no matter how small. Progress in real estate isn’t always about the number of sales—it’s about understanding the story those numbers tell.